The subject of money is weighing on the minds of many Americans. Some 2 in 5 U.S. adults say that money issues negatively impact their mental health, according to a new survey by Bankrate.

That should probably come as no surprise, as inflation continues to hover at 40-year highs, but the most common cause of that distress might be: not enough emergency savings.

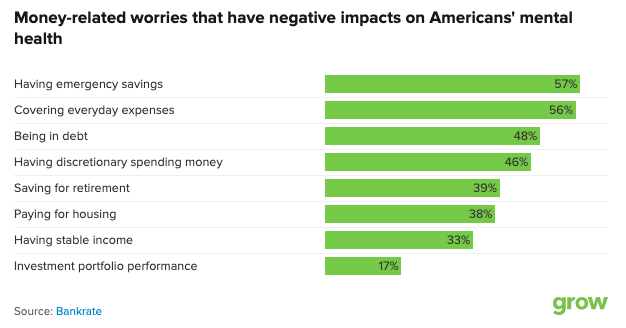

Of the eight categories respondents could choose from to describe the main source of their financial worries, nearly 3 in 5, or 57%, said that not having enough emergency savings played a role.

Nearly the same percentage, 56%, said that not being able to pay everyday expenses came in close second at 56%.

Source: Bankrate

The fact that not having emergency savings came in as Americans’ No. 1 financial worry shouldn’t be surprising, says Mark Hamrick, senior economic analyst at Bankrate.

“Our surveys traditionally have indicated the number one financial regrets are the failure to save for emergencies and the failure to save for retirement,” Hamrick says. Over the years, “those have been hard to knock out of that top spot.”

Money relates to your mental health in a big way

What did surprise Hamrick, however, was that financial worries were the second highest cause of distress among Americans, second only to global events.

“Financial issues are essentially on par with some of the biggest challenges that we face when it comes to our mental health,” Hamrick says. “When you look at those other factors that people were judging against or comparing, like world events or physical health, [financial issues] are basically, on par with those. I thought that was quite stunning.”

It’s a reminder that economic issues like inflation and rising interest rates hit real people in real ways, Hamrick says.

As for the top two categories for financial worries, it makes sense that they’re about saving for emergencies and paying for everyday necessities, he says.

“They could be viewed as two sides of the same coin, right? One way that you might be dealing with extraordinarily high inflation is to dip into emergency savings,” Hamrick says.

The personal savings rate, the amount of income that people store for a rainy day, reached record highs during the pandemic, but as inflation remains stubbornly high, those gains from the past few years are starting to ebb, Hamrick says. “We have seen savings coming down, and there’s increased utilization of credit card debt.”

To boost your savings, automate them

Many financial professionals agree that one of the best ways to stay smart about saving is to automatically have a certain percentage of your paycheck or other deposits go into a savings account. Once that is set, it not only means little to no work on your part, but also means you can almost forget that it’s even happening.

“You don’t have to do a lot,” said Marguerita Cheng, a CFP and founder of Blue Ocean Global Wealth. “Even $25 or $50 per paycheck” is a good start.

That’s because, thanks to compound interest, those $25 or $50 can add up to something big over time, especially if that money goes into a high-yield savings account.

Try our compound interest calculator to see for yourself!

Plus, with time, “what was uncomfortable becomes more comfortable,” Cheng says, and you can go from saving smaller amounts to bigger ones.

This material has been presented for informational and educational purposes only. The views expressed in the articles above are generalized and may not be appropriate for all investors. The information contained in this article should not be construed as, and may not be used in connection with, an offer to sell, or a solicitation of an offer to buy or hold, an interest in any security or investment product. There is no guarantee that past performance will recur or result in a positive outcome. Carefully consider your financial situation, including investment objective, time horizon, risk tolerance, and fees prior to making any investment decisions. No level of diversification or asset allocation can ensure profits or guarantee against losses. Article contributors are not affiliated with Acorns Advisers, LLC. and do not provide investment advice to Acorns’ clients. Acorns is not engaged in rendering tax, legal or accounting advice. Please consult a qualified professional for this type of service.

Gabriel Cortés was a reporter and data journalist for Grow.